Credit Union Helps Employees Navigate Student Loans

Duke Credit Union seminar covers repayment, consolidation, forgiveness

Lance Boland juggles loans for an undergraduate degree, teaching certificate and ultrasound training. He's paying the private loans but deferred payment on two federal loans until next April.

"I'm trying to figure out all my options and find out what has changed since I started borrowing a decade ago," said Boland, an ultrasonographer in the Duke Hospital Neurodiagnostic Lab.

Read MoreFor help sorting through loan solutions, Boland recently attended "Student Loan Repayment," a seminar through the Duke Credit Union about loan repayment, consolidation and forgiveness options. He was interested in learning more about a new federal program, Public Service Loan Forgiveness, which offers loan repayment assistance for borrowers working in public service.

The seminar was attended by more than a dozen Duke employees and led by Sherrie Clayton, accounting manager for the Duke Student Loan Office.

"There have been a lot of changes recently in the student loan world," Clayton said. "It pays to pay attention to your loans and stay informed about your payment options."

Boland said the seminar helped him understand additional research to conduct for his specific situation. "My plan is to look into consolidating my federal loans in the New Year and see if the public service forgiveness is an option for me," he said.

Clayton offers the following advice on handling student loans.

Know who holds the loans. In the economic turmoil of the past few years, banks sold many loans to other banks, and in 2010, the federal government began offering all new loans under the Federal Direct Loan program. Borrowers can track all federal loans on the National Student Loan Data System. Private bank loans can be monitored through credit reports available free at www.annualcreditreport.com. "It's important to know who you are working with, especially if you have questions," Clayton said.

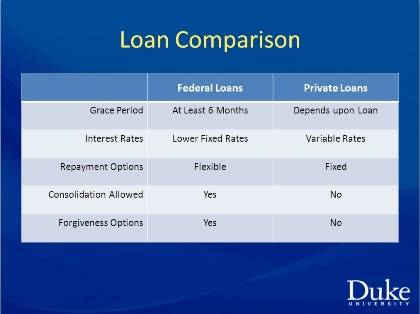

Understand payment options. Federal loans offer a variety of payment options, including the standard fixed payments over 10 years, an extended 25-year option and a 10-year graduated option that allows a borrower to increase payments over 10 years. "There are pros and cons to each plan," Clayton said. "You generally can't change the interest rate on a federal loan, but when circumstances change, it may be possible to adjust your payment plan," she said.

Stay informed. The federal government periodically creates new programs to assist borrowers in paying loans. One example is the Income-Based Repayment plan for borrowers whose student loan debt is high relative to income and family size. Borrowers with older federal loans can consolidate them into one loan to take advantage of this plan. The government provides an online calculator to help borrowers estimate if they are eligible for this program.

Know the rules of forgiveness. The federal government will often cancel a portion of the loan if a borrower enters the military, Peace Corps or other federal program, or if a borrower has made 25 years of on-time payments. Through the Public Service Loan Forgiveness program, borrowers may qualify for forgiveness of the remaining balance due on certain loans after 10 years of payments made while employed full time in a public service job. "Public service includes universities and health care so some jobs at Duke would be covered under this program," Clayton said. Detailed information is available on the Federal Student Aid website.

Consider consolidation carefully. Consolidating loans may make bookkeeping easier. "But consider this option carefully, because you can only consolidate federal loans once and sometimes when you consolidate, you lose flexibility," Clayton said. For example, if a borrower consolidates a federal Perkins loan with another loan, he or she may lose some eligibility for forgiveness later in the life of the loan.

Avoid Default. In September of 2011, the federal government said the official student loan default rate had risen from 7 percent in 2008 to 8.8 percent in 2009. The consequences of default can include having money withheld from wages, having a professional license withheld and loss of eligibility for future federal financial aid and loan deferments. Clayton said a loan goes in default when a payment is 270 days past due. "If you are having problems paying, you should talk to your loan officer before those 270 days are up," she said.